The Clause That Rewrites Your Cap Table

27 May 2026 · 8 min read

Milan Bilimoria

Milan BilimoriaMost founders who have raised institutional capital have an anti-dilution provision in their shareholder agreement. Most of them have never modelled what it does.

That is not a criticism of the founders. Anti-dilution provisions sit in a section of the shareholder agreement that feels theoretical at the point of signing: a protection for an investor against a scenario that, at the optimism of a freshly closed round, feels remote. The company is growing, the round just closed, the next milestone is in sight. A down round feels like someone else’s problem.

In Q1 2025, over 19% of all funding rounds were down rounds, a figure that has remained elevated since 2023 and is notably higher than anything seen between 2019 and 2022. One in five rounds. For the founder sitting across from an investor today, a down round is not a remote theoretical scenario. It is a realistic outcome that deserves to be modelled before the term sheet is signed.

This piece is about what happens to your cap table when it does, and why the version of the anti-dilution provision you agreed to determines whether the outcome is manageable or severe.

What anti-dilution provisions are actually doing

When a company raises a new round at a lower valuation than a previous one, the investors from that previous round have paid more per share than the new investors are paying. Their ownership percentage, already diluted by the new shares being issued, is further undermined by the fact that they overpaid relative to the current market price. An anti-dilution provision compensates them for that by adjusting the price at which their preferred shares convert into ordinary shares, giving them more shares at conversion than they originally received.

Think of it this way: you paid £4 for a cinema ticket last month. This month the same cinema is selling the same seat for £2.50. Anti-dilution is the cinema giving you extra tickets to make up for the difference. The question is how many extra tickets they give you.

The provision does not change the cash already invested. It changes the number of shares the investor receives when their preferred shares convert, which directly affects every other shareholder’s ownership percentage. Every additional share issued to the investor under anti-dilution is a share that dilutes the founder and everyone else on the cap table.

There are two versions of this term and the difference between them is not a matter of degree. It is a matter of kind.

Broad-based weighted average

Broad-based weighted average anti-dilution, referred to as BBWA, adjusts the investor’s conversion price using a formula that takes into account the size of the down round relative to the total shares outstanding. The adjustment is proportional: a small down round at a modestly lower valuation produces a modest adjustment, and a large down round at a severely lower valuation produces a more significant one. The formula weights the new lower price against the existing share base, which means the investor is compensated in proportion to the actual economic impact of the down round rather than receiving the maximum possible compensation regardless of circumstances.

It’s like splitting a bill fairly after one person ordered less than expected. Everyone adjusts, but the adjustment reflects what actually happened, not the worst case scenario.

BBWA is the market standard in the UK. It is the version founders should be pushing for in every term sheet, and it is the version most institutional investors will accept because it reflects a reasonable and proportional protection of their position without extracting disproportionate value from the founder in a moment of difficulty.

Full ratchet

Full ratchet anti-dilution takes a different approach entirely. It adjusts the investor’s conversion price to match the new round price exactly, regardless of how large or small the down round is, how many shares were issued at the lower price, or what proportion of the total cap table the new round represents. A single share issued at a lower valuation triggers the full ratchet for the investor’s entire position.

Using the same analogy: full ratchet is the cinema giving you free tickets for every film showing that week because one seat sold cheaper on one day. The compensation has no relationship to the actual loss.

The consequence of this is significant. Because the conversion price drops to match the new round price in full, the investor receives a much larger number of additional shares than they would under BBWA, and those shares come at the direct expense of the founder’s ownership. The math is unforgiving, and it does not require a dramatic down round to produce a painful outcome.

Full ratchet provisions are rare in UK seed term sheets but they exist, and they tend to appear in rounds where the investor has significant leverage: a founder with no competing term sheets, a round that has taken longer than expected to close, or a company that has accepted structured terms in exchange for getting the deal done. They are worth identifying and negotiating against before the term sheet is signed, not after.

What this looks like in practice: Priya’s round

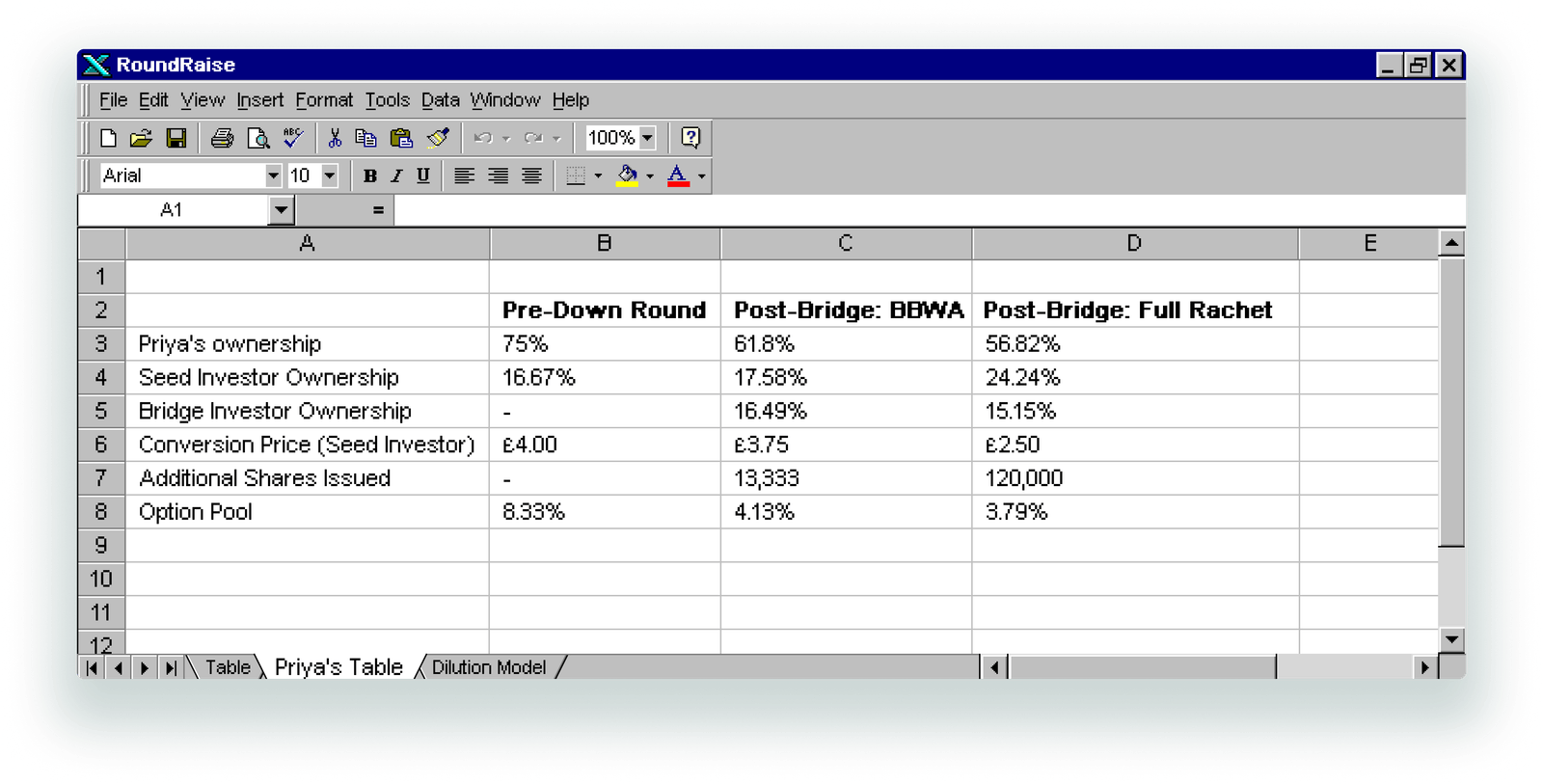

Priya raises an £800k seed round at a £4m pre-money valuation, in line with the UK market median for seed rounds in 2024. Her seed investor takes 16.67% of the company post-money. After a 10% option pool created pre-money at seed, which Priya absorbs in full, she holds 75% of the company. The seed investor holds 16.67%. The option pool accounts for the remainder.

Eighteen months later, growth has slowed. The Series A Priya expected to raise is not coming together at the valuation she anticipated. She needs a £500k bridge round to extend runway and hit the metrics that will make the Series A possible. The best terms available are a £2.5m pre-money valuation, a 37.5% drop from the seed round.

The down round triggers the anti-dilution provision. What happens next depends entirely on which version Priya agreed to.

Under BBWA, the seed investor’s conversion price adjusts from £4.00 to £3.75 per share. They receive 13,333 additional shares at conversion. Priya’s ownership after the bridge closes sits at 61.8%.

Under full ratchet, the seed investor’s conversion price drops to £2.50, matching the bridge round price exactly. They receive 120,000 additional shares at conversion. Nine times as many as under BBWA. Priya’s ownership after the bridge closes sits at 56.82%.

The difference is 4.98 percentage points of founder ownership, produced not by anything Priya did or did not do operationally, but by a single word in the shareholder agreement she signed at seed.

Imagine you own 75 of 100 shares in a jar. Under BBWA, someone adds 13 new shares to the jar and gives them to the investor. You now own 75 of 113. Under full ratchet, someone adds 120 new shares. You now own 75 of 220. Same jar. Same down round. Completely different outcome.

At a £30m exit, the difference between 61.8% and 56.82% is approximately £1.5m in founder proceeds. At a larger exit it compounds further. And this is modelling a single seed investor with a single anti-dilution provision. Founders who have multiple investors with anti-dilution rights face a version of this calculation for each one simultaneously.

What to do about it

The anti-dilution provision is negotiable at the point of signing and almost impossible to renegotiate after. The ask is not that founders reject anti-dilution provisions entirely: they are a standard and reasonable investor protection and most institutional investors will not proceed without some form of them. The ask is that founders understand which version they are signing and push back firmly if the term sheet specifies full ratchet rather than broad-based weighted average.

BBWA is market standard in the UK. If an investor presents full ratchet as a standard term, it is not. A well-advised investor knows this, and a founder who pushes back with reference to market standard, supported by their lawyer, has a reasonable basis for negotiation. Accepting full ratchet without negotiating is accepting the worst case version of a term that has a perfectly reasonable alternative built into market practice.

Beyond the type of provision, founders should also understand whether their anti-dilution protection applies to all investors or only to the lead. In rounds with multiple investors, anti-dilution provisions that apply to every participant can produce a compounding dilution effect in a down round that is significantly more severe than modelling a single investor in isolation would suggest. Knowing who has anti-dilution rights, in what form, and what the combined effect of all of them looks like in a realistic down round scenario, is the kind of modelling that should happen before the first term sheet is signed rather than after the first difficult quarter.

At RoundRaise, we build tools that help founders understand what they are signing before they sign it. If you want to model your own anti-dilution scenarios across both BBWA and full ratchet, you can find us atroundraise.co.uk.

We also have afounder wall . It’s a public board where founders leave notes, share lessons, and say the things they wish someone had told them earlier. If you’ve been through a down round, or you have a view on the terms that caught you off guard, it belongs there.