What Kiran's Exit Actually Paid Out

17 June 2026 · 9 min read

Milan Bilimoria

Milan BilimoriaEvery piece we have published in this series has been about a single instrument, a single term, or a single structural decision. SAFEs, ASAs, convertible notes, option pools, liquidation preferences, anti-dilution provisions, term sheet mechanics. Each one examined in isolation, with its own scenario and its own modelled numbers.

The problem with that approach is that none of these things exist in isolation. They sit on the same cap table, they interact with each other at exit, and the moment that determines what a founder actually receives for building their company is the moment all of them arrive simultaneously. That moment is the exit waterfall, and most founders have never seen one modelled in full before they are sitting in a room watching it happen to them.

This piece does that modelling. We are going to follow one founder, Kiran, through three rounds of funding, build his cap table precisely at each stage, and then run the exit waterfall at two different exit valuations to show exactly where every pound goes and why.

As the HSBC Innovation Banking Venture Capital Term Sheet Guide notes: if a founder hasn’t done their waterfall modelling, doesn’t know what to look out for, and hasn’t appreciated the risks embedded in the deal structure, that can leave them receiving a payout far less than they expected. This piece is the modelling most founders never do until it is too late to change anything.

Building Kiran’s cap table

Kiran starts with 100% of his company. He is a solo founder, no co-founder split, no prior equity issued. From that starting point, three rounds of funding reshape the cap table before the exit arrives.

Pre-seed: £150k ASA at a £1.5m post-money cap

Kiran’s first raise is an ASA, the instrument we covered in detail in our last piece. He raises £150k from a UK angel at a £1.5m post-money valuation cap. The angel’s ownership is fixed at signing: £150k / £1.5m = 10%. Kiran retains 90%. No interest accrues, no maturity date creates pressure, and the investment is SEIS compatible, which means the angel is claiming tax relief on their capital at risk.

At this point the cap table is simple. Kiran owns 90 shares in every 100. The angel owns 10. Nothing has converted yet because there has been no priced round.

Seed: £600k priced round at £4m pre-money

The seed round is a priced equity round. This is the qualifying event that triggers the ASA conversion. Before the new investment is priced, two things happen: the ASA converts into ordinary shares, and a 10% option pool is created pre-money.

The option pool is created first. On a pre-money basis, 111,111 new shares are issued to the pool before the seed investor’s price per share is calculated. Kiran absorbs this dilution in full; the incoming seed investor does not. After the pool creation, the total share count is 1,111,111 shares. The seed investor’s price per share is £4m / 1,111,111 = £3.60. At £600k, the seed investor receives 166,667 new shares.

After the seed round closes, the cap table looks like this:

-

Kiran: 900,000 shares / 70.4%

-

Angel (ASA converted): 100,000 shares / 7.83%

-

Seed VC: 166,667 shares / 13.04%

-

Option pool: 111,111 shares / 8.7%

-

Total: 1,277,778 shares

Kiran started with 100%. After one angel round and one seed round with an option pool, he owns 70.4%. He has raised £750k in total. The dilution feels gradual because it arrived in two separate events, but the cumulative effect is a 30% reduction in his ownership before he has taken a penny of Series A capital.

Series A: £1.5m at £8m pre-money, 1x non-participating liquidation preference

The Series A brings institutional capital and the first liquidation preference on Kiran’s cap table. Before the new investment is priced, a second option pool top-up is created pre-money, bringing the total pool to 10% of the post-top-up share count. This requires issuing 141,975 new shares to the pool, which Kiran absorbs again.

The Series A investor’s price per share is £8m / 1,419,753 = £5.634. At £1.5m, they receive 266,312 new shares.

After the Series A closes:

-

Kiran: 900,000 shares / 53.38%

-

Angel (ASA): 100,000 shares / 5.93%

-

Seed VC: 166,667 shares / 9.88%

-

Series A VC: 266,312 shares / 15.79%

-

Option pool: 252,086 shares / 14.95% (original plus top-up, assumed unissued for modelling)

-

Total: 1,686,065 shares

Kiran now owns 53.38% of his company. He has raised £2.25m in total across three rounds. The Series A VC holds a 1x non-participating liquidation preference on their £1.5m investment, which means they will receive £1.5m before any proceeds are distributed to ordinary shareholders, unless converting produces a better outcome.

The exit waterfall at £8m

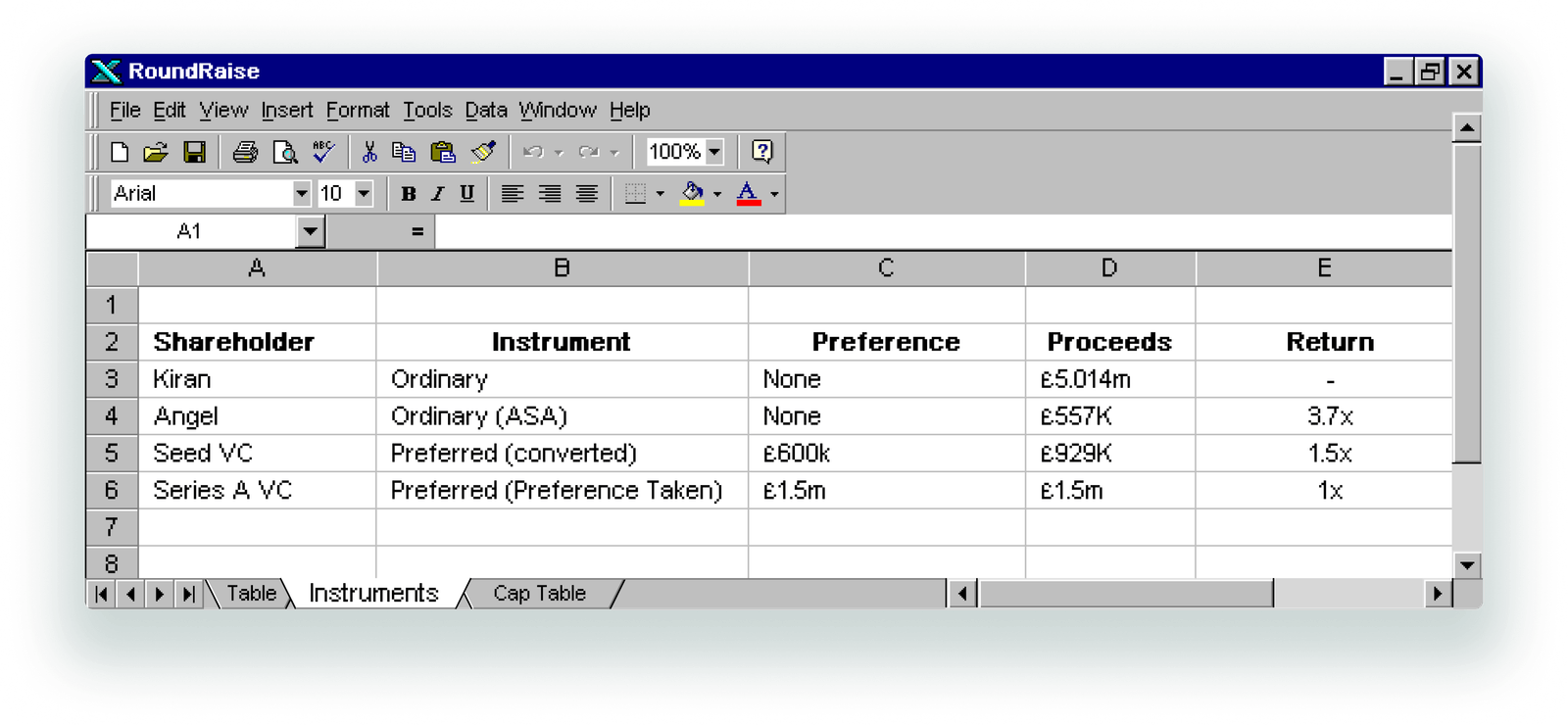

Three years after the Series A, Kiran receives an acquisition offer of £8m. It is a solid outcome; not exceptional, but a meaningful return on the capital and years invested. The question is not whether it is a good exit. The question is what each shareholder actually receives when the proceeds are distributed.

The waterfall runs in sequence. Liquidation preferences are paid first, before any ordinary shareholder receives anything.

Step 1: Series A VC decision

The Series A VC holds a 1x non-participating preference of £1.5m. They have a choice: take the preference, or convert their preferred shares into ordinary shares and participate pro rata in the full £8m.

Converting would give them: 15.79% × £8m = £1.263m.

Taking the preference gives them: £1.5m.

They take the preference. £1.5m is paid to the Series A VC immediately. £6.5m remains.

Step 2: Seed VC decision

The Seed VC holds a 1x non-participating preference of £600k on their remaining £6.5m pool. Converting would give them: 9.88% of the remaining £6.5m after the Series A preference = approximately £642k.

£642k exceeds their £600k preference, so they convert. They participate pro rata in the £6.5m alongside Kiran and the angel.

Step 3: Pro rata distribution of remaining £6.5m

The remaining pool is distributed among ordinary shareholders: Kiran, the angel, and the Seed VC (who has now converted).

-

Kiran: 900,000 / 1,166,667 = 77.14% × £6.5m = £5.014m

-

Angel: 100,000 / 1,166,667 = 8.57% × £6.5m = £557k

-

Seed VC: 166,667 / 1,166,667 = 14.29% × £6.5m = £929k

-

Series A VC: £1.5m (preference, already paid)

Kiran receives £5.014m from an £8m exit. That is 62.7% of the total proceeds, which is close to his ownership percentage of 53.38%. The reason he receives a higher percentage than his ownership would suggest is that the Series A VC took their preference rather than converting, which removed their pro rata claim from the remaining pool and left more for everyone else. A well-structured liquidation preference, in a modest exit, can actually work in the founder’s favour.

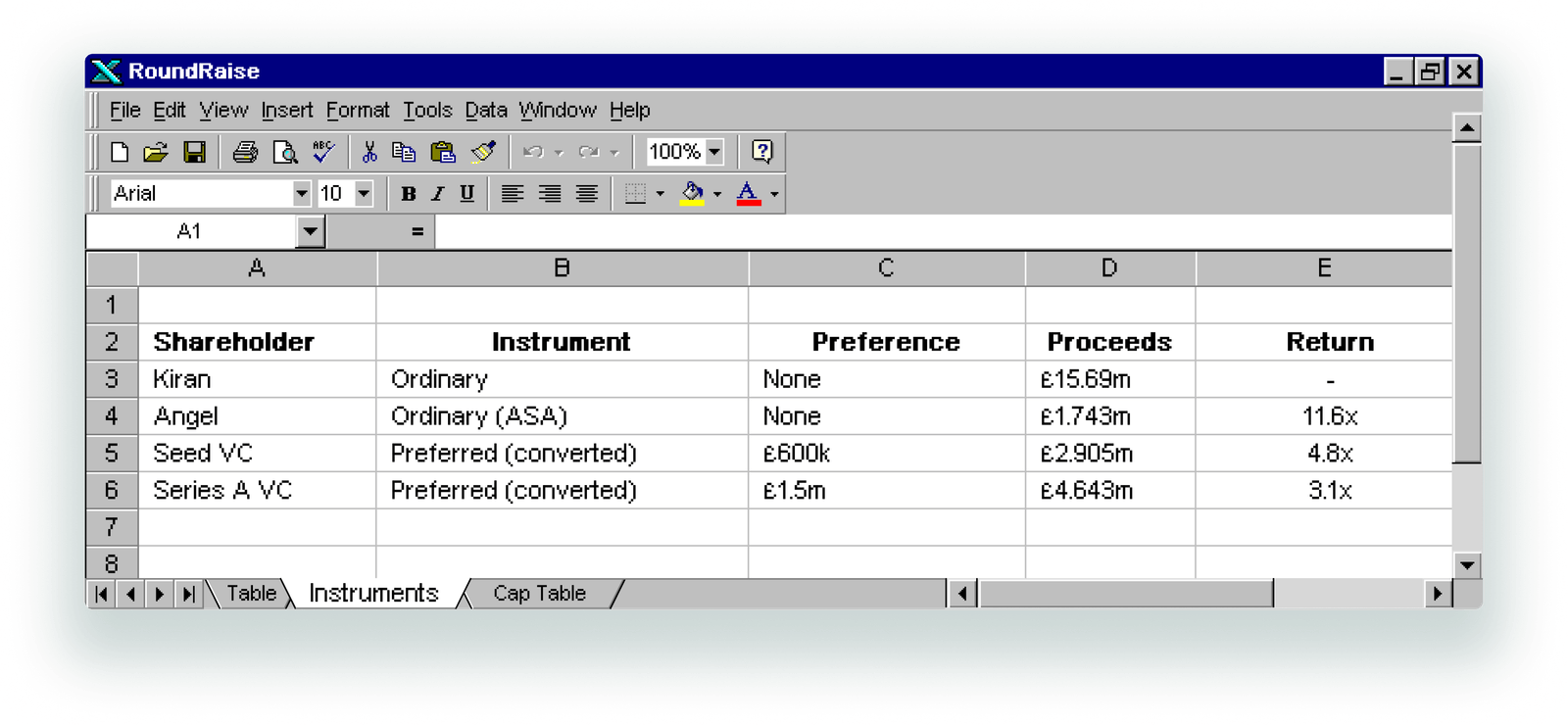

The exit waterfall at £25m

Two years later, a larger acquirer makes an offer of £25m. The same cap table, the same preferences, but a materially different outcome for every line of the waterfall.

Step 1: Series A VC decision

Converting gives them: 18.57% × £25m = £4.643m.

Taking the preference gives them: £1.5m.

They convert. No preference is paid. The full £25m is distributed pro rata.

Step 2: Seed VC decision

Converting gives them: 11.62% × £25m = £2.905m.

Taking the preference gives them: £600k.

They convert. Full pro rata distribution.

Step 3: Full pro rata distribution of £25m

-

Kiran: 62.76% × £25m = £15.69m

-

Angel: 6.97% × £25m = £1.743m

-

Seed VC: 11.62% × £25m = £2.905m

-

Series A VC: 18.57% × £25m = £4.643m

At £25m, the preferences disappear entirely because every investor does better by converting than by taking their preference. The waterfall becomes a simple pro rata distribution. Kiran receives £15.69m, which is 62.76% of the proceeds, almost exactly matching his ownership percentage. The structure that mattered enormously at £8m is irrelevant at £25m.

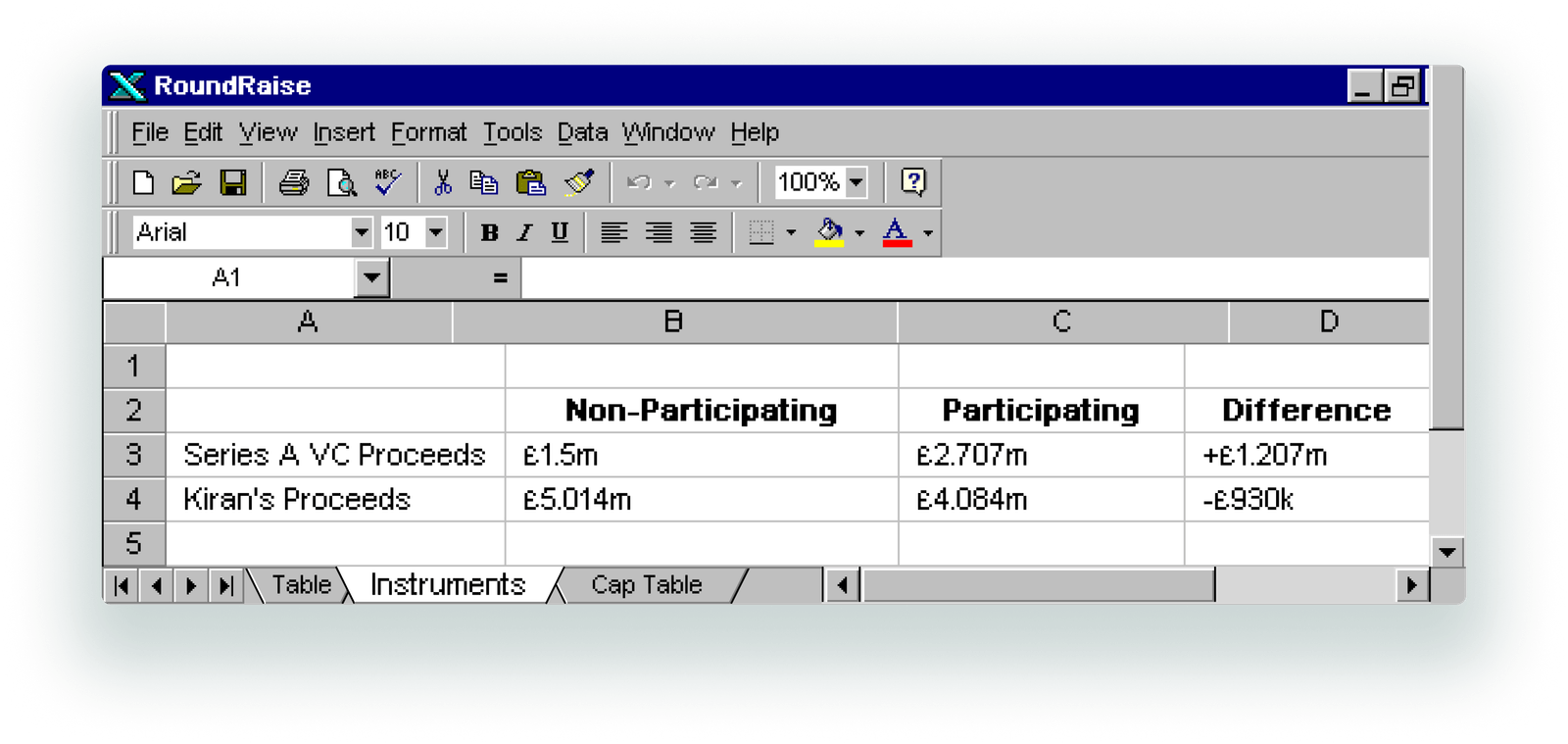

The word that changes everything

Everything above assumes a 1x non-participating liquidation preference for the Series A investor, which is UK market standard. One word change in the term sheet, from non-participating to participating, produces a materially different outcome at the £8m exit.

Under a 1x participating preference, the Series A VC takes their £1.5m preference and then participates pro rata in the remaining proceeds alongside ordinary shareholders. They get paid twice.

At the £8m exit:

-

Series A VC takes £1.5m preference first

-

Series A VC then takes 18.57% of the remaining £6.5m = £1.207m

-

Series A VC total: £2.707m

The remaining pool after Series A participation: £5.293m, distributed pro rata among Kiran, the angel, and the Seed VC.

-

Kiran: 77.14% × £5.293m = £4.084m

-

Difference to Kiran vs non-participating: £930k less

One phrase. Participating versus non-participating. At an £8m exit, that single term costs Kiran £930k. Not because anything went wrong with the business. Not because the valuation was wrong or the round was poorly structured. Because one clause in one term sheet allowed the investor to extract value from two places simultaneously at the moment of exit.

In 2024, 97% of non-participating preference shares carried a 1x multiple, reflecting the market standard that most institutional investors accept. The participating preference is the minority term. But it is the term that costs founders the most when it appears, and it appears precisely in the rounds where founders have the least leverage to push back on it.

What the waterfall teaches you

The exit waterfall is not a document you look at once and file away. It is a model you should be running continuously from the moment you take your first institutional capital, at every exit valuation that is realistic for your company, under every combination of preference terms on your cap table.

The numbers above are not hypothetical. They reflect the structure of a realistic UK early-stage company that has raised sensibly, taken market-standard terms at each round, and built a clean cap table. Kiran is not a cautionary tale. He is a founder who did most things right. And yet the difference between a 1x non-participating and a 1x participating preference at his Series A is £930k at an £8m exit, produced by a single clause agreed in a room where he was relieved to have a term sheet at all.

The waterfall does not care about the circumstances in which the terms were agreed. It runs the calculation mechanically, in the sequence the documents specify, and distributes the proceeds accordingly.

Model it before you sign. Model it again before you exit. The numbers will tell you things the term sheet did not.

At RoundRaise, we build tools that help founders run this modelling before the exit conversation begins. If you want to model your own exit waterfall across different scenarios and preference structures, you can find us atroundraise.co.uk.

We also have a founder wall atapp.roundraise.co.uk/board — a space where founders leave the things they wish they had known earlier. If you have been through an exit and have something worth leaving there, we would be glad to have it.