What You Would Do Differently the Second Time

3 June 2026 · 8 min read

Milan Bilimoria

Milan Bilimoria

There is a version of fundraising knowledge that cannot be taught in advance. It arrives through the experience of having done it once, made the decisions that felt right at the time, and then watched those decisions play out across the years that followed. Every founder who has raised twice carries a set of things they would do differently, and almost none of those things are about the pitch.

They are about the structure. And in the UK specifically, where the gap between what founders accept and what the market could offer them is wider than most people realise, getting the structure wrong in the first raise is a more expensive mistake than it looks at the time of signing.

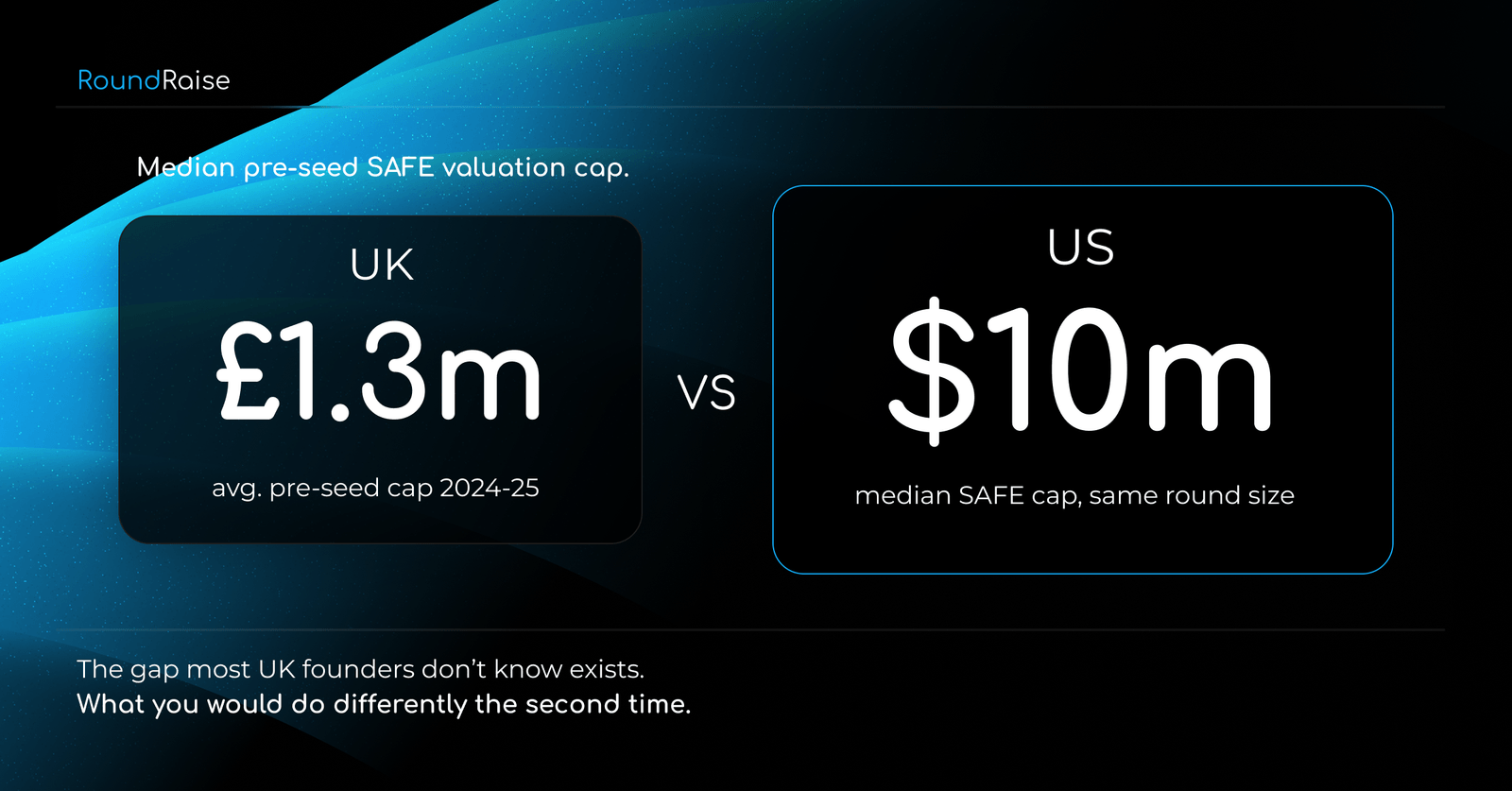

Consider the numbers. UK pre-seed valuations averaged £3.2m in 2024-2025, with SAFE caps commonly sitting in the £2m to £5m range. In the US, the median valuation cap on a post-money SAFE for a round of the same size was around $10m. That is not a marginal difference. It is a structural gap that reflects a different investor culture, a different risk appetite, and a different set of expectations about what an early-stage company is worth before it has proved anything. UK founders raising at the lower end of that range are not necessarily accepting bad terms because they negotiated poorly. They are often accepting the terms that the market offered them without knowing that the market was offering them less than they might have been able to push for.

Then layer onto that the timeline. The journey from seed to Series A in the UK now takes an average of 29 months, up from 18 months in 2019. The decisions made in a thirty-minute conversation with an angel at pre-seed are decisions that will sit on a cap table for nearly two and a half years before the next institutional round gives anyone an opportunity to reset them. Most first-time founders do not have that context when they sign. The ones who have been through it once already do.

Here is what the second raise changes.

You raise for 29 months, not 18

The eighteen-month runway figure has been repeated so many times in accelerator programmes, investor blog posts, and founder communities that it has acquired the status of a rule rather than a heuristic. It made sense when seed to Series A took eighteen months. It does not make sense now, and the founders who discover this mid-raise rather than before it are the ones who end up doing a bridge round on worse terms than they would have accepted at the original close.

The second time, you build the runway calculation around the actual timeline rather than the conventional one. That means raising more than feels strictly necessary, accepting more dilution upfront in exchange for the security of knowing you will not be back at the table in a position of weakness eighteen months from now, and modelling the Series A milestone not as a twelve-month sprint but as a twenty-four to thirty-month journey with setbacks built in.

The practical consequence of this is that the amount you raise at seed should be determined by what the milestones actually require, not by what feels like a reasonable ask given current traction. A founder who raises £400k thinking they can get to Series A readiness in eighteen months and finds themselves at month twenty-two with six months of runway left is not in a position to negotiate. They are in a position of necessity, and investors can tell the difference.

You are far more selective about who sits on your cap table

In the UK, where institutional pre-seed capital is concentrating upward and most first raises happen through angel stacks rather than single-lead rounds, the cap table that results from a first raise often reflects the order in which people said yes rather than a considered view of who the founder actually wants around the table for the next three years.

The second time, you understand what that cap table costs. Every angel with pro rata rights is reserving space in your Series A allocation. Every investor with information rights is receiving updates that create an ongoing obligation across a growing list of people. And the fragmentation of having eight or ten angels each with a small stake and no formal lead is something every institutional investor will read carefully when they look at your cap table for the first time. It does not disqualify you from raising, but it creates friction that a cleaner structure would not.

None of this means turning down good people or good money. It means being intentional about who you invite in and what you are offering them. The second time, founders tend to think about the cap table they are building rather than the round they are closing, and those are meaningfully different frames for the same set of decisions.

You set the cap with the Series A in mind, not the current conversation

This is the decision that the UK market makes hardest to get right the first time. When the reference points around you are caps of £1.5m to £3m, when the angel sitting across from you is used to investing at those levels, and when the alternative to accepting the offered cap is potentially not closing the round at all, the structural implications of a low cap are easy to deprioritise in the moment.

But a pre-seed cap is not just a number that determines what your angel receives at conversion. It is the first data point in a valuation narrative that will need to hold together across every subsequent round. A Series A that comes in at £9m pre-money tells a very different story if the pre-seed cap was £1.5m than if it was £4m. In the first case, the step-up is 6x, which is a strong signal of progress. In the second, it is 2.25x, which is a modest increment that some institutional investors will probe. The cap you set in a first raise determines the baseline from which every subsequent valuation is measured, and that baseline follows you.

The second time, founders tend to push harder on the cap conversation, not because they have more leverage, but because they understand what they are actually setting when they agree to a number. They know that a cap of £1.3m for £150k means giving away 11.5% of their company at a valuation that will make the Series A story harder to tell, and they weigh that cost against the relief of closing the round with more clarity than the first time allowed.

You read the term sheet before you feel grateful for it

This is the hardest one to explain to someone who has not yet been through the experience of raising for the first time, because it requires understanding a feeling that only the experience itself produces.

When the term sheet arrives, after months of conversations, rejections, silences, and near-misses, the relief is overwhelming. And relief is the worst possible emotional state in which to review a legal document. It creates a powerful incentive to treat the term sheet as a verdict to be accepted rather than a negotiating position to be engaged with, and that incentive is strong enough that most first-time founders sign terms they would have pushed back on if the document had arrived under different emotional circumstances.

The second time, you have enough distance from that relief to read the term sheet as what it is. You know that participating preferences are not UK market standard and can be negotiated. You know the difference between broad-based weighted average and full ratchet anti-dilution and why it matters in a down round. You know that the option pool size is not fixed and that a hiring plan is a legitimate basis for negotiating it down. You know that good leaver and bad leaver definitions vary considerably across term sheets and that the definition of bad leaver is worth reading carefully before you agree to it.

None of that knowledge makes the negotiation comfortable. But it makes it possible. The term sheet is the moment when those conversations can happen. The shareholder agreement signing two weeks later is not.

The gap between a first raise and a second one is not really a knowledge gap. Almost everything above is learnable before you raise. The real gap is one of context: the ability to make structural decisions with a clear view of their long-term consequences rather than in the immediate emotional context of trying to close a round in a market that is harder than you expected and takes longer than you planned for.

The UK market in particular rewards founders who have that context before they need it. The timeline is longer, the caps are lower, and the distance between what you accept and what you could have pushed for is wider than in almost any other major startup ecosystem. Getting the structure right the first time is harder here than anywhere else. But it is also where it matters most.

At RoundRaise, we build tools that help first-time founders make those decisions with the same clarity that experience eventually provides. You can find us at roundraise.co.uk.

We also have a founder wall atapp.roundraise.co.uk/board, a space where founders leave the things they wish they had known earlier. If you have been through a raise and have something worth leaving there, we would be glad to have it.